Peeping in at the corners of the U.S. CRE financing problems — rates too high, banks wary to lend, refinancing tough to get — are the various rising costs of commercial real estate properties. Expenses that act like a pry bar, pulling profit out of a property’s NOI.

Rising insurance premiums and lower levels of coverage are more than an anecdote here and there. In January 2024, the Federal Reserve’s Beige Book noted a comment out of the Kansas City Fed: “Some contacts suggested that transaction activity may pick up slightly in coming months as appetites for restructuring loans may increase after year end. Yet, falling rents and rising insurance costs adversely affecting net operating incomes remained widely cited concerns inhibiting loan restructuring when desired.”

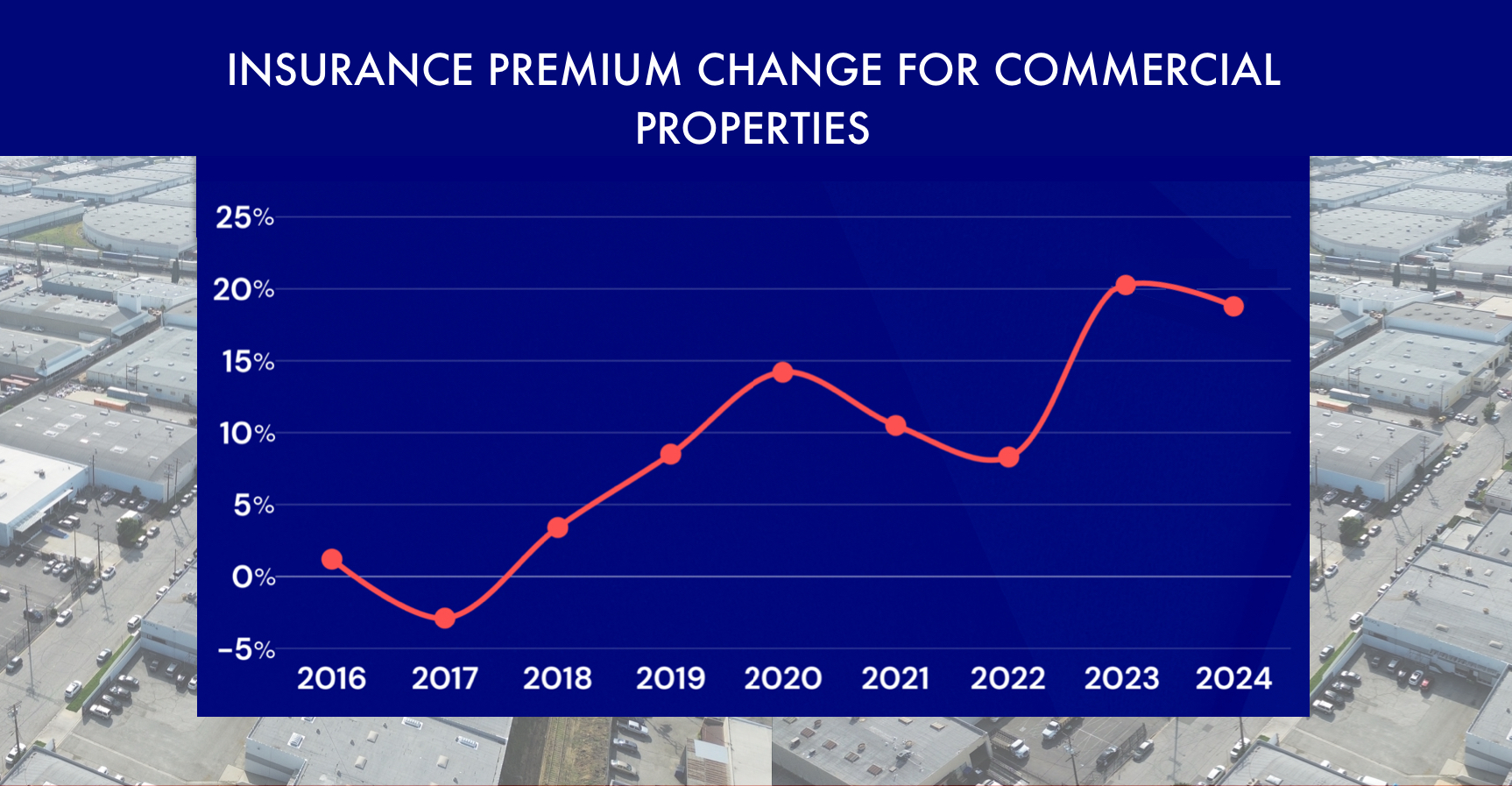

In July 2023, Moody’s Investor Service calculated that for CRE, insurance had risen by 73% over the previous five years. Commercial property insurance premiums hit a record rise of 20.4% in the first quarter of 2023. It was the first time since 2001 that rates had jumped more than 20%. Premiums were rising by double digits in many markets. Some policy renewals offered half the coverage for that same price they had the previous period.

The lack of affordable options was putting needed levels of coverage out of the reach of owners. Yardi reported that states with increasing climate-related risk, such as Florida and Texas, see their costs rising upwards of 50% and starting to threaten new development and property sales.

At the time, Brett Forman, managing partner at Forman Capital, said, “I got an email yesterday from a fund I’m personally invested in. They didn’t have claims. Their insurance costs have risen by 70%. That changes the cash flow dynamics. It’s a big line item.”

Things haven’t improved since then, according to an article from Business Insurance. During an Arthur J. Gallagher & Co. real estate and hospitality webinar, Justin Dove, San Francisco-based area vice president at Gallagher, said that even the basics aren’t evolving with the market. Limits and deductibles in policies often haven’t been updated in years.

Historical damage amounts have doubled or quadrupled without policies recognizing it. Martha Bane, Glendale, California-based senior managing director of the North America property practice at Gallagher, said that 70% of the global $123 billion in damage “came from what are considered as either lightly modeled or nonmodeled perils”. Severe weather is affecting areas that never had experienced it before and so aren’t properly modeled.

Source: https://www.globest.com/2024/02/06/ensuring-success-with-spiraling-insurance-prices/