The market for small-bay industrial properties, those spanning 10,000 to 100,000 square feet, is still pretty tight but showing signs of easing. Availability is 6.4%, well below the 10.9% rate for the broader logistics market, as steady leasing that’s largely in line with pre-pandemic norms has combined with historically limited construction to keep vacancy in check in recent years. Yet conditions are beginning to shift as elevated economic uncertainty weighs on small businesses and curtails expansion plans, particularly for newly completed space.

According to the April 2026 NFIB Small Business Economic Trends report, the Uncertainty Index remains well above its historical average, reflecting persistent concerns about inflation, weakening sales expectations and a more cautious broader economic outlook. As a result, fewer small business owners consider this a good time to expand, and growth expectations have deteriorated.

While roughly 17% of the small businesses in the Index still plan to make capital outlays, that share remains below prior demand-cycle highs, and many small businesses are delaying or scaling back investment decisions. Instead, firms are prioritizing cost controls and pricing adjustments, deferring expansions until economic visibility improves.

Previous strong demand for new supply begins to fade

For industrial real estate, this pullback is translating into softer near-term demand for newly constructed small-bay space. Small businesses, the primary tenant base for this building type, are less inclined to expand, relocate or lease additional space. This shift is already showing up in leasing trends. The availability rate for small-bay properties that are currently under construction has risen from below 40% before 2023 to more than 53% today, reflecting weaker pre-leasing across the pipeline. The sharp increase over the past year aligns with rising business uncertainty and a pullback in capital expenditure plans within the small business segment. By contrast, existing small bay industrial space has been more resilient. Availability for stabilized properties has increased only modestly, rising from a cyclical low of 3.8% in mid-2022 to 6.4% today.

Performance gap between new and existing stock grows

Looking ahead, elevated economic uncertainty, higher operating costs, and reduced demand are likely to further widen the gap between newly completed small bay industrial space and existing inventory. Since 2024, the years of available supply for small-bay properties built since 2020 has increased from less than 1.5 years to 2.7 years. If demand weakens further, that figure could approach three years by the end of 2026, signaling growing lease-up risk for recent deliveries.

Meanwhile, older properties, particularly those in infill locations closer to a small business’s client base, are likely to maintain tighter availability. While new developments offer modern specifications, including higher clear heights, they are often located in less central areas, requiring customers to drive farther and use more fuel to reach them.

Location advantage supports older inventory

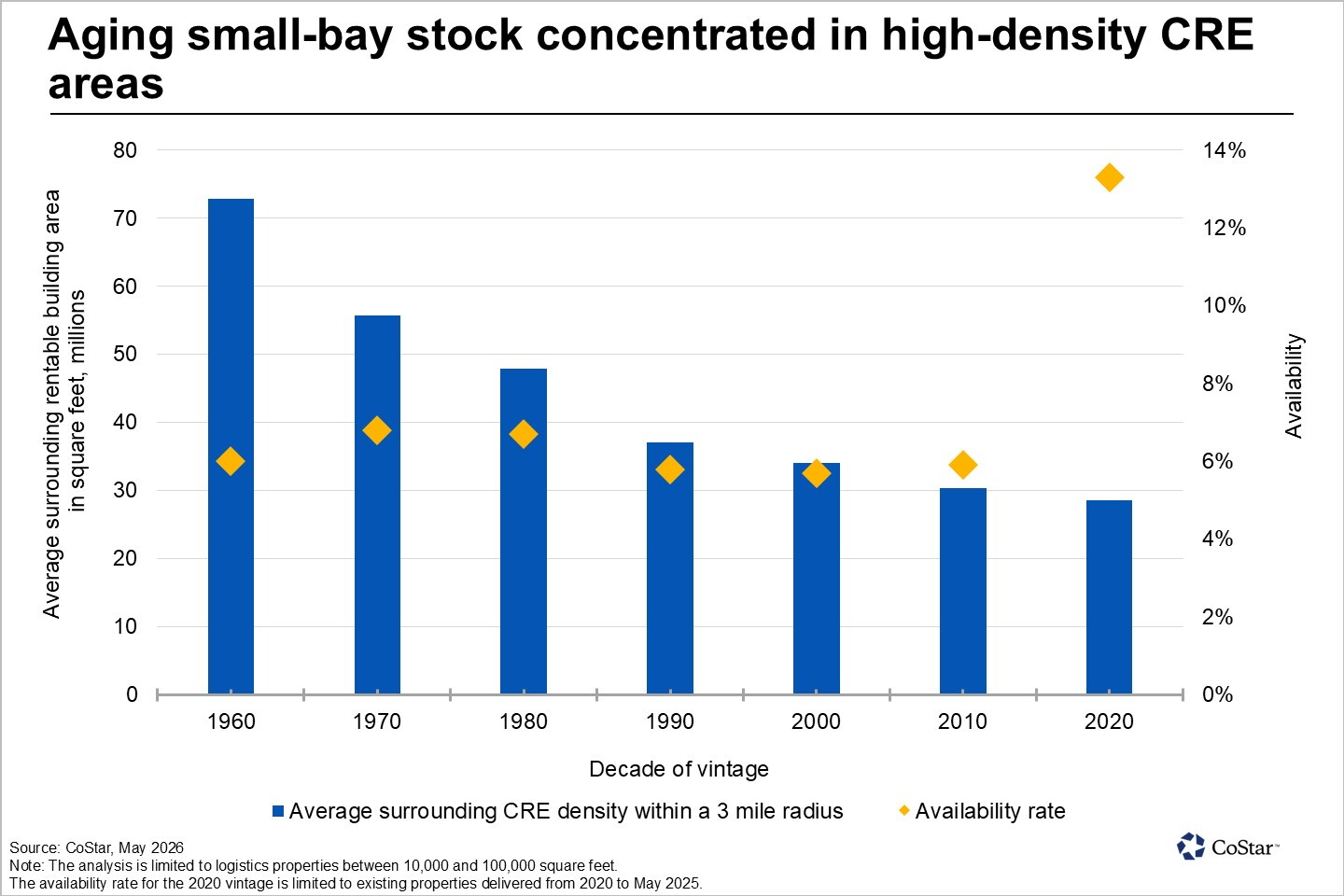

Small-bay properties built before the 1980s are generally located in significantly denser commercial environments, surrounded by more than twice as much nearby commercial real estate as newer developments. This locational advantage continues to support sub-7% availability rates for older small-bay inventory, well below the more than 13% rate for properties built since 2020 and far below the elevated vacancy levels among projects nearing completion. In addition, the supply of legacy small-bay inventory continues to shrink. More than 52 million square feet of small-bay industrial space built before 2000 has been demolished since 2015, often redeveloped into higher-density uses. This ongoing attrition is further tightening the supply of infill space and enhancing the relative scarcity of older assets.

With inflationary pressures continuing to weigh on small business margins, proximity to customers remains a critical advantage. Lower transportation costs and faster service times are reinforcing demand among this segment for infill locations, helping older small-bay properties maintain occupancy despite significant rent increases in recent years.

Sources: https://www.nfib.com/wp-content/uploads/2026/05/NFIB-SBET-Report-April-2026.pdf, https://product.costar.com/home/news/940465019